On February 2, in a small town in Punxsutawney, Pennsylvania on Gobbler’s Knob, an unsuspecting furry Groundhog is plucked from a burrow to predict the weather for the rest of the winter. When the groundhog sees his shadow, the belief is that North America will experience an additional six weeks of winter. In contrast, in keeping with the Pennsylvania Dutch tradition, if the groundhog does not see his shadow, the forecast is for an early spring.

The 1993 movie Groundhog Day made this tradition famous. The movie storyline focuses on Phil Connors (played by Bill Murray), a bitter newscaster, trapped in a time loop forcing him to relive the February 2nd groundhog viewing over-and-over again. As a result, the term Groundhog Day is synonymous for a person reliving a series of repetitive, and monotonous events.

I feel the pain. Today, I hosted the monthly call for the Network of Networks group. During the period of 2016-2020, we hosted quarterly events, and monthly calls, to encourage inter-operability testing between network providers and the building of open canonicals to automate supply networks. On this morning’s call, we reflected on progress. I was asked the question, “Why did we not make more progress in the past six years in driving inter-operability between networks?” When I heard the question, I felt Phil Connor’s pain. My Groundhog Day experience was real.

The call to action to form the Network of Networks Group in April 2016 was:

The start of the Network of Networks Share Group April 2016Increasingly companies are evaluating business network solutions to close the gap on inter-enterprise visibility; but as companies work on the problem, they find that they need to somehow interconnect business networks. The gaps are large. Defining a solution to close the gaps are not so easy.

It is time to bring Manufacturers, Retailers, and Distributors together with Technology Providers in order to better understand the issues and generate ideas to help build the “network of networks.”

The group did make some progress. We sponsored the ISO standard 88705 for corporate authoritative identifiers termed the Authoritative Legal Identifier (ALEI). (With the evolution of tax efficiency initiatives, we found that the average company had more than 150 legal identities, but that they could be used to track flow.) The European group tested blockchain concepts. Together, we validated the gaps in blockchain platforms for supply chain automation.

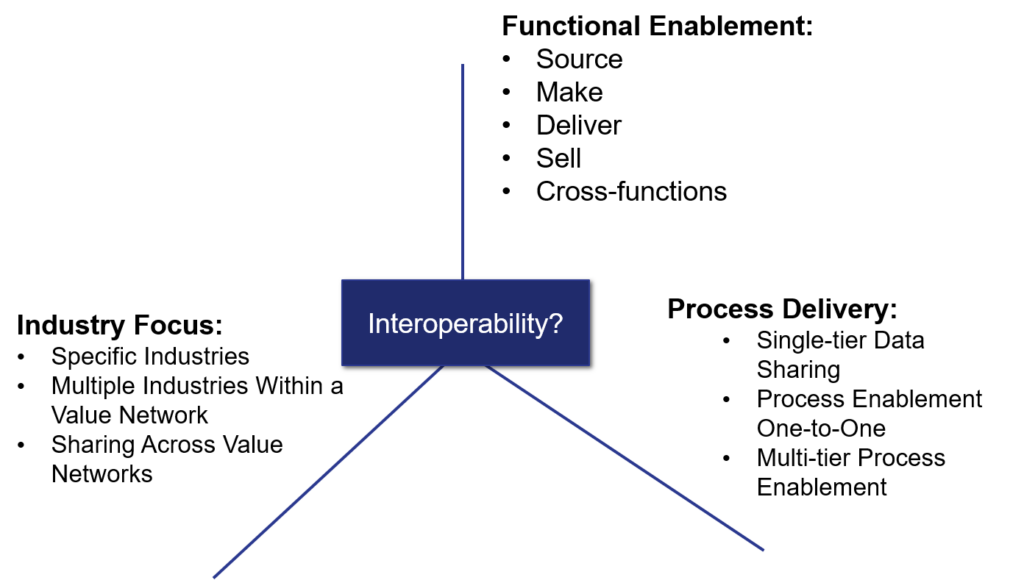

Over the six years, the forum did provide active networking and sharing of information on standards adoption and improvements for existing networks. Today, I select a guest speaker working on network innovation and share research. It is a safe space for business and tech leaders to talk openly on how to improve outcomes, but I did not achieve my original goals. We did not make progress on driving interoperability between the multiplicity of networks shown in Figure 1.

Figure 1. Flavors of Networks

Today, only 8% of multi-tier data flows through one-to-many or many-to-many networks while 29% is based on Electronic Data Interchange (EDI). The balance moves through spreadsheets and email. As a result, there is no system of record to synchronize changes, and the data takes one-to-three days to move from node to node. (Brand owner to contract manufacturer or third-party logistics provider to a retailer.) This data latency, and the lack of synchronization, results in network blackholes. (A blackhole is an astronomical term where the pull is so great that no matter escapes.) This is one of the primary issues in improving network visibility.

Barriers Leading to My Groundhog Day

I answered the question attributing the lack of progress to seven factors:

- Brand Owner Vacuum. Short of the initial launch of B2B exchanges in 2002, in the period, no brand owner drove the adoption of network technologies. The most knowledgeable teams that manage multi-tier information sit 4-5 layers down in an organization. I find few business leaders have improving network capabilities and flow on their agendas. Many still believe that network automation starts with the implementation of Enterprise Resource Planning (ERP) or that they have to wait for perfect data. (Both assumptions are false.)

- Industry Held Hostage by ERP Upgrades. Let’s be clear, no company is letting grass grow under their feet. The industry focus for the past three decades on Enterprise Resource Planning (ERP) consumed capital and energy. The industry is caught in an endless cycle of ERP upgrades. As ERP architectures morphed to include portals, the unknowing believed that this could become a connector for network infrastructure. No ERP provider drove open network architectures.

- Education. The term network is used frequently, but without definition. The term value is also used a lot, but without definition. In a project that I am currently working on with Georgia Tech, I had a bet that the research assistants would not find a clear definition for value network in the literature. They were sure that they would find it. Sadly, I won this argument. Value networks, like many supply chain terms, are used frequently, but lack definition. As shown in Figure 1, there are many types of networks: industry-focused networks, functionally focused networks (like sourcing and logistics) and specialized networks for discovery (marketplaces), product serialization, open innovation. I count over a hundred public networks in the market today with no interoperability. I know of no-means to drive interoperability across make, source, and deliver in a multi-tier network.

- Technology Evolution. In 2002, I was a Gartner analyst covering the evolution of network technologies in supply chains. At that time, I followed a boom-and-bust cycle for trading exchanges. Great ideas, but the concepts were ahead of technology capabilities. Today, the opposite is true. The evolution of network concepts in biology, and physics along with the evolution of technology capabilities of ontological frameworks and the graph makes this a different discussion. Currently, I am focused on the F# work at the Max Planck Institute in Berlin. I know of nothing similar in the United States where we are emersed in technobabble of generative AI to improve the planning engines in Advanced Planning (APS) taxonomies (YAWN). (In my opinion, inside-out planning processes are so yesterday.)

- Decline in Innovation Due to M&A. The network solutions have been through a series of vicious M&A cycles. EDI networks consolidated. Thoma Bravo hallowed-out the Elemica, Exostar, and GHX assets while Insights enabled a M&A buying spree of enterprise solution assets at E2open. Trimble bought Transporeon. Infor bought GT Nexus, SAP purchased Ariba and Kinaxis acquired MPO. In all cases, innovation declined. The greatest innovation occurred in the use of Internet of Things (IoT) data for transportation in solutions like Four Kites, Project 44, and Transvoyant, but each faces the same issue. There is no place to put and use the IoT data effectively in current Enterprise architectures.

- Business Models. By definition, the existing commercial models of network solution providers do not enable the building of interoperability between and among networks. The bridges to drive data across networks will only happen if the technology providers are forced to make this switch by either government intervention or brand owner dictates. However, I question is this will ever happen because there is a lack of understanding of the difference between integration and interoperability in the industry. As a result, synchronization, and harmonization of data is stripped away with the semantic layer.

- Consortia Consolidation. Over the decades, I watched the consolidation of industry groups. The merger of Food Marketing Institute (FMI) and Grocery Manufacturers Association (GMA) could have created a collaborative space to build network solutions. Instead, the group was hijacked by manufacturers trying to make the group a big brand selling opportunity to retail. The merger of Edgell Communications with Consumer Goods Technology (CGT) forums and Path to Purchase Institute had a similar outcome. Similarly, the Foundation for Strategic Sourcing, originally founded by brand owners, now has only a few brand owner participants becoming a sales vehicle for contract manufacturers and third-party logistics providers. As a result, there are no safe spaces for trading partners to build and test multi-tier process networks.

Deep sigh on this Groundhog Day.

I find it ironic that there is so much talk about environmental action (ESG) but so little investment in networks. Too few realize that more than 70% of the impact to the planet is in the network. I was hopeful, that recent ESG focus would accelerate the investment in networks. And, as people better understood network automation that they would realize that the enterprise investments, that they are so proud of, are ineffective in building effective networks. But, alas, the current investment cycles continue down narrow roads limiting our ability to make a step change in environmental impact. I guess we will continue to plant trees. At least groundhogs like trees…

So, happy Groundhog Day! I am going to hang out and have a cold one with Punxsutawney Phil. Maybe tomorrow will be better.

As always, I would love your thoughts.

What do you think? Why are we not enabling network transformation projects?