I was sitting with a representative from the United Nations on my way back from Colombia. As we took off from Bogota, we discussed the potential of blockchain to help her with feeding children in the highlands of the Colombian-Venezuelan border. I was surprised that she knew enough about blockchain to have a discussion, and I think that she was surprised to find someone who could help her to have a deeper discussion. Today I connected her to some technology providers to start a pilot.

This morning I read a Wall Street Journal article on blockchain asking “Why Is Blockchain Not Hotter?” I smiled as I read the article, thinking about the random-chance of meeting a United Nations representative on a Delta flight who hungered to test blockchain. Through my work with the Network of Networks group, several things are becoming apparent. I think I know why blockchain is not hotter. Here are my thoughts:

1) A Lot to Figure Out. For Example, What Is a Node? Blockchain is a piece of a larger technology platform. It is critical to define the publish/subscribe mechanisms, the data architecture, and think through the nodes. Blockchain is a decentralized system based on nodes. The nodes enable replication and authentication of the data. We are not clear on which companies should be a node and how to architect public data sharing across the supply chain.

2) Security in Many-to-Many Architectures. Most of the blockchain work today is one-to-many, not many-parties-to-many-parties. Supply Chain Operating Networks like Elemica, GT Nexus (now Infor), and SAP Ariba are many-parties-to-many-parties. The complexity of many-to-many networks, as compared to one-to-many operating networks, is different by an order of magnitude. Security and data management in many-to-many architectures, and the management within blockchain, is still experimental.

3) Organizational Readiness. We are not set up to test. People with a deep understanding of EDI are in different organizations than the business teams. In most organizations they do not know each other. Companies want definitive ROIs. Power brokers–companies with significant buying power–are not stepping up to the plate (with the exception of Maersk and Walmart).

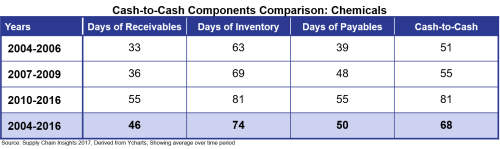

4) We Have More Sticks than Carrots. While supply chain leaders talk about collaboration, over the last decade processes steadily pushed cost and waste backwards in the supply chain. The cost of doing business is much more expensive for companies four and five layers back in the value network. For example, receivables and payables steadily increased in the chemical industry.

These are my thoughts. I welcome yours!

We will be discussing these topics, and many more, at the upcoming Supply Chain Insights Global Summit on September 5-8, 2017. We hope to see you there!

The Tale of the Gartner Supply Chain Planning Magic Quadrant and Minestrone Soup

Self-congratulations notes abounded this week as vendor-after-vendor shared their rankings on the Gartner Magic Quadrant for Supply Chain Planning. For me, it was a big